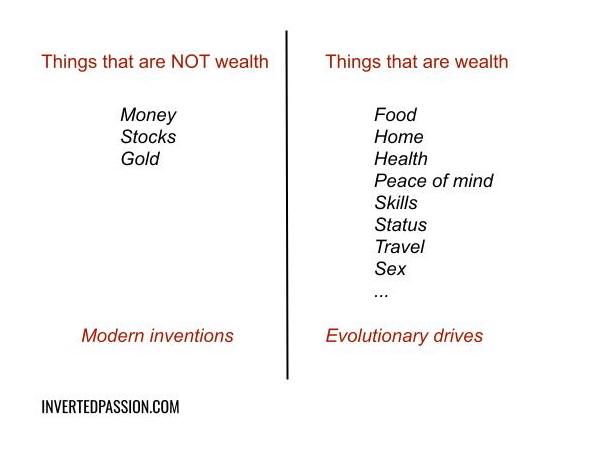

As an entrepreneur, money is obviously a massive motivation for why you’re doing what you’re doing. However, it’s essential to understand that money is not wealth.

The reason money is so popular because it allows us to acquire (certain types of) wealth. Money will be worthless if what you desire cannot be bought, or if there’s nothing you desire. Because most of what we desire can be had for cheap in modern society, the importance of money in our society is reinforced by people who are excessively driven by status. ...Read the entire post →

I recently finished this excellent short book titled What Has Government Done To Our Money. It’s available on the Internet for free and I highly recommend reading it. But in case you want the key insights, here are my notes.

Money as a medium of exchange

1/ In an economy, there’s a variety of people. Different folks specialize in producing different things and each one of them desires different things.

2/ If there are only two people, they can barter (i.e. directly exchange) what each one of them has with what the other one needs. Even with two people, an exchange rate emerges (e.g. how many loaves of bread you both agree on for a pair of shoes?) ...Read the entire post →

If you follow me on Twitter, you’d know that I’ve been working on a trilogy of short films on climate change. Funded by Wingify, these films are a collaboration between me (writer) and Robert Grieves (animator). We’re calling this initiative Wingify.earth.

The first short film is out now and it’s about relationship between money, climate change and entropy (a concept which I elaborated on in a previous essay on this blog). Watch the 3 minute film below and leave your comments on its Youtube page....Read the entire post →

Post-docs (people with PhDs who aren’t professors yet) get an average of $52k of salary per year. Librarians and postal service works get $55k and $57k respectively. I came across these figures on an angry blog post where the author concluded:

The hard truth is academic postdocs are not valuable.

Why are intelligent people who’ve spent five or more years making an original contribution to the world (PhDs) paid less than people who’ve done short vocational training (librarians, mailmen)?

Scientists are selfish

Scientists are paid less because they’re doing it for their own pleasure. The topics they choose to work on are the ones that they’re most passionate about. But markets don’t pay people for indulging – in fact, there’s a cost for indulgence. Academics pay that cost by losing on the money they could have gotten in the industry. And, in industry, they seldom chose to select their topic of interest. There’s no free lunch!

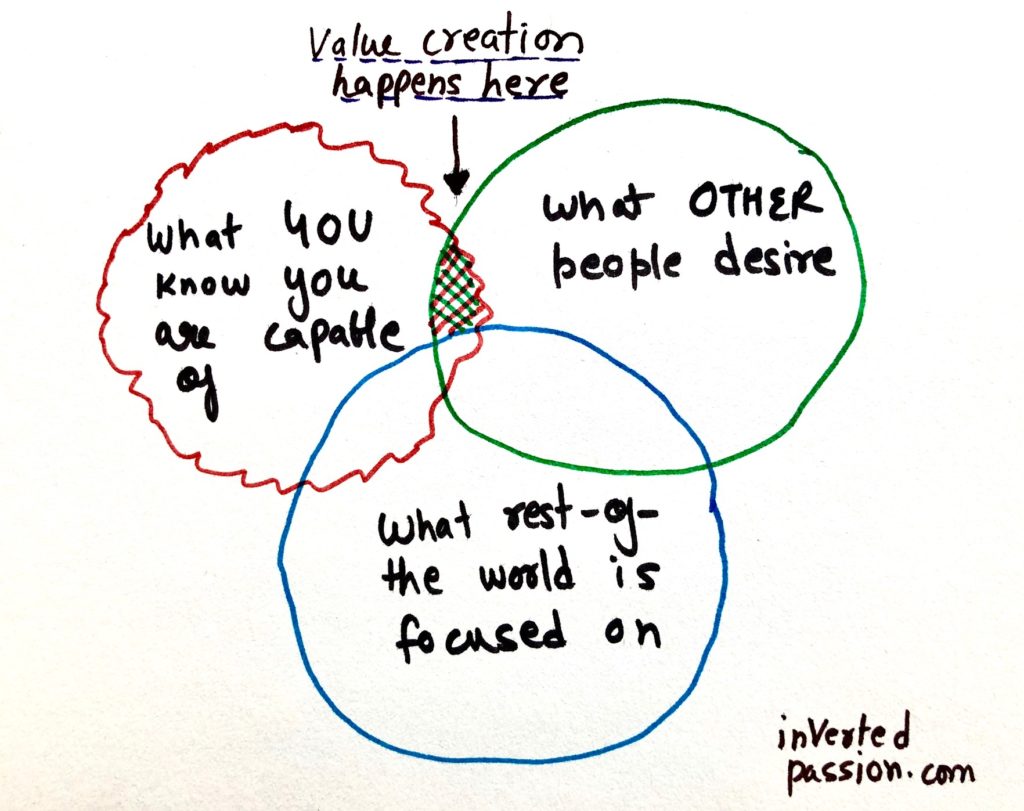

It’s different for librarians and mailmen because they make fulfill someone else’s needs and the market pays them for that. This website is called Inverted Passion because value creation starts with finding out what others are passionate about and then adapting yourself to service their needs and desires. To create value, passion usually needs to be inverted.

The Inverted Passion model

Science is a positive externality

Externalities are (beneficial or harmful) consequences that happen to someone was not part of a transaction. An example of negative externality is pollution. If making soap increases a firm’s profit but pollutes water, it typically continues doing that. Health impact on the public is an externality. Such negative externalities could remain unchecked for a long period of time because no single individual is harmed directly and immediately. Pollution kills slowly so nobody is incentivized to invest time and money to get the factory to shut down. In such cases, government regulation (in terms of pollution tax or shutdown notices) is required.

Science in a similar way helps the humanity collectively. A knowledge published in a research paper belongs to everyone. Because it’s beneficial, it’s a positive externality. But the market doesn’t value it because detection of the first interstellar object in our solar system does little to change how an average human goes about his/her life daily. This is why governments step in to fund science. However, that comes with a host of problems.

The amount of science funding is not enough

Talking about scientists and mailmen, in 2015 the revenue of United States Postal Service was $68 Bn while the total funding for science made available by US government was $30 Bn. Let that sink in. The money flowing through the mail industry in US was more than twice the money flowing from government to science.

The lesson for profit seeking entrepreneurs is to let go of their passion and instead seek what other people value. It sounds obvious but our inside-out view muddles thinking and we mistakenly start thinking other people have a need for something we’re building out of passion. (Psychologists call it the mind-projection fallacy) I’ve made that mistake several times in my career. I let my passion guide me and I built things that nobody wanted.

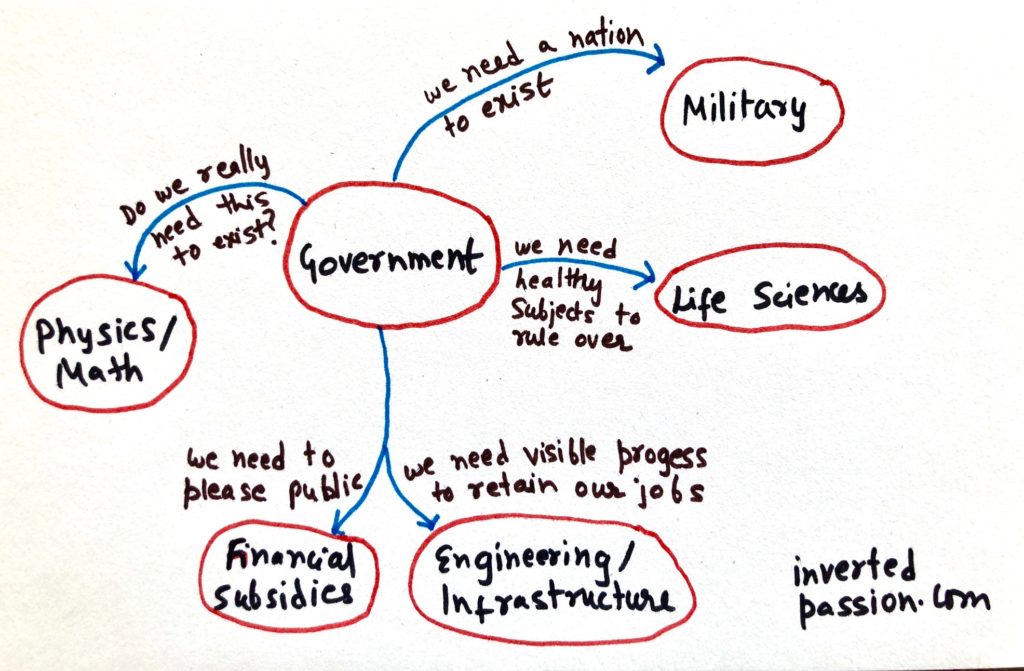

Government spends in areas where it’s incentivized to do so

In 2015, the US government spent $600 Bn on military while it spent 1/20th of that on science. In fact, for some politicians this $30bn might be too much. Quoting from the Scientific American:

Some members of the new Congress have already vowed to cut all nonmilitary R&D.

It’s important to note that governments do not spend evenly across scientific disciplines. Life sciences, engineering and environmental sciences get most of the funding while physics, mathematics and psychology get much less. (And if you’re doing research in social sciences, good luck to you).

This uneven distribution of funding happens because governments are incentivized to show progress in metrics that the majority of humans care about – that is things that about what immediately benefits him/her in the short term. Scientific disciplines that have indirect or long term benefits lose out. The verification of Higgs Boson will not help the government get re-elected, so it doesn’t (easily) allocate funds towards that. However, because government officials must protect their jobs, they must have a nation that funds them so it easily approves of thousands of military research projects.

Incentives in a system drive behaviour in that system

Limited funding = hunger games in academia

The academia is not a utopia. Being a professor is grueling. The professor has to write research proposals, beg for grants and navigate a highly political environment. To understand why academia is political, first, let’s note that it is a non-market environment. In a (capitalistic) market, money measures the amount of value created. But academia is structured differently and because

market does not reward professors and academics with big money ...Read the entire post →

I wanted to make money by myself and was pretty happy when people paid for the first version of VWO. I remember my goal was to make roughly USD 1000 (equivalent of the last monthly salary I had drawn at my employer). VWO ended up making me multiple times my initial goal.

Last month at Wingify, we hit a million dollars of recurring revenue. I’m very happy that the team has been able to achieve this milestone, especially because we’re entirely bootstrapped and haven’t raised any outside investment. There has been a lot of enthusiasm about the million-dollar-a-month figure, and all Wingifighters are pumped up to convert the ‘m’ into a ‘b’. Amidst all this, I want to take a moment to reflect on what really is money.

Is billion dollars enough money? How about a trillion dollars?

This question sounds strange because common sense immediately tells us: ‘of course, a trillion dollars is a big amount’. Imagine all the things one could buy with a trillion dollars – islands, space ships and perhaps even Switzerland. It’s indeed a lot of money.

Let’s pause for a moment and think how fascinating it is that the world will let you buy stuff and anything else you want just because your conversion rate optimization platform and website push notifications system exist. I realize that I’m stretching the point a bit, but hang on with me for a moment.

What amazes me is this: if you had a billion dollars, you’d most probably never have a physical sensation of that money. You can’t keep it in your drawer, you can’t hold it, you can’t physically posses it. In fact, it is very likely that your billion dollars don’t even exist. Nobody has it. US Fed (as of 2016) says $1.46 trillion of cash is in circulation, while debt in US is more than $19 trillion (as of 2016). If everyone in US decides to physically possess the money they have, they will fall short of more than $17 trillion.

What’s happening here?

Ultimately,

Money is a promise that in future you will be able to claim the equivalent of value that you’ve created today

Who makes this promise? The government (but any mutually trusted 3rd party can do that; like in case of bitcoins where people put trust in blockchain).

Why we need a future promise in terms of money?

We require the idea of money because of two reasons:

Simple barter works where I make shoes and you make wheat. We exchange those objects and each one of us is happy. However, money is needed because a single individual is typically able to create far more value than s/he can consume personally. Larry Page and Sergey Brin created far more value in the world with the PageRank algorithm than their personal lifetime wheat and food requirements. Money is required for a fair exchange of value.

Simple barter may also work when I have a need for shoes right now and I’m willing to give you wheat. But what if I had a blockbuster wheat production this season, but don’t really want equivalent-value 10 pairs of shoes? In such cases, money is needed to store the value so the possessor is able to utilize it in future for something else.

Where does money derive its worth? Why is 1 dollar same for everyone?

One way to answer this question is to ask: ‘when does the other person decide to give you one dollar’. You get one dollar from others when you provide one dollar of value to them. Seems cyclical, but it isn’t. Imagine that you have a roadside stand with a banner that says: ‘Stuff for $1’. First, you put out a piece of crumbled paper on that stand and wait for customers. People come and go, they notice, but nobody buys. You wonder why is that so. After all, $1 is not a lot of money. You get frustrated and are just about to throw the crumbled paper into the trash before you spot an art collector running towards you with a $100 bill. She begs you to sell this piece of art to her and you, amazed, say why not. Being generous, you ask her if he wants 2 more crumbled papers free with that and he immediately backs off and asks you to sign an agreement that you will never make any more crumbled papers.

All this amazes you. Nobody wanted to pay $1 for a crumbled paper, but before you almost gave up, someone came up and bought it for $100. Not just that, she said she won’t buy it unless you promise not to create any more crumbled papers.

1921 Rolls Royce for $1. Any takers? Photo from FrankDale

You then put out your second item for the $1 sale – this is your vintage 1921 model Rolls Royce. It’s the only one remaining in the world as the company has stopped making them. The minute you put keys + car’s photo on the stand, you see a rush of people, each with a dollar bill in hand trying to buy the car from you. Such a huge rush of people makes you anxious and you decide to go inside and catch a breath (and drink some lemonade). By the time you come back, you see someone offering you $10,000 for something you wanted to sell for $1. Before you knew, BBC covers this and you get an offer of $1 million from an unknown source. You had a thing for lots of zeros, so you immediately take the offer and hand over the keys.

What just happened? Why did someone gave you a million dollars when you actually wanted to just sell it for $1?

Why did the world make Wingify a million-dollars-a-month company when all I wanted to make was $1000?

The answer lies in this: money is a proxy for how much value you create for other humans

Money, be it a dollar, a million, billion or trillion dollars, is ultimately a proxy for amount of value you are creating in the world.

Someone decides to hand you X units of money because you provide them with X units of value. It’s as simple as that.

Watch the video on how economic machine works. I promise it’ll be the best 30 minutes you will spend today

How is additional money created?

In most cases, economies are zero-sum games. You get $100 for doing a job, you spend $90 on pizzas, video games and movies and put $10 in your bank. The $90 that you spent is someone else’s income (which they further spent, so no new money is created in a transaction), and $10 that you put in your bank is lent to someone who must give back $11 to the bank. If the economy was just limited to $100, where does this extra $1 in the come from?

What I’m talking about here is not money-as-cash (which is easy to create – just print additional money). Here, I’m talking about money-as-value. If most economic transactions are just exchange of value, where does additional value come from? The answer lies in the question: the additional money-as-value is created in the world when additional value is created in the world.

Economic growth happens when more of human needs are satisfied. Chart from Economist

Let me give you an example. Suppose that in pre-Industrial age, you are in a sweater manufacturing business, making sweaters by hand and are the only one selling sweaters in the town. The maximum you are able to make are 10 sweaters a day, putting in $5 worth of wool and sell them for $10 each, making your daily profit of $50. Your limited capacity means that you are able to sell sweaters only to a limited number of people in your town. Some of them are able to buy, the others are left wanting. This inability to serve more people frustrates you because your money making potential is limited and you really want to see more people wearing your sweaters. So you set out to invent a machine to make sweaters.

After years of toiling on the part time, you see success – finally a machine that can make 100 sweaters in a day. You take a loan to get more wool and start producing sweaters. You are cautious first and only make 20 sweaters on day 1. Much to your surprise, even though you have 20 sweaters to sell, you are still only able to sell 10. People who didn’t buy tell you that while they’d love to buy sweaters, they have already spent all their savings on stuff they are used to paying for. They simply don’t have additional money to buy your sweaters. Next day you figure out that if you sell sweaters at a cheaper price, say $8, selling 20 of them will still make you a total of $60 daily profit – more than what you made before.

You slash your price to $8 and this is when value is created. People who had $10 budgets for your sweaters buy it for $8 and spend the remaining $2 on stuff that other people are selling. After buying all the stuff that they are used to buying, the other people now have an additional $2 to spend and in 4 days each one of them is able to buy your sweater. You give some part of $60 daily profit as interest to the loan you took but are still left with more daily profit than what you had before ($50). You have more money, your people in town are able to afford more sweaters. When everybody wins, it’s not a zero sum game and additional money-as-value is created in the world.

Money is created when you are able to satisfy more (or equivalent) of human needs while using equivalent (or less) resources and time. The freed up resources and time is then used to do other stuff that people value.

In other words, productivity drives economic growth. People value a lot of things – efficiency, leisure time, finding mates, being engrossed, mastering a skill. Satisfying all those needs using lesser resources than before (through technology, innovative policies, newly discovered resources) is how additional value is created.

Startups are in the business of creating value for others

Today’s startups are a world apart from the simple theoretical barter system of economy. The dot com hype of 1999 sent startups to stratosphere, where many of them IPOed and made lots of money for their founders and investors. Then they came crashing down and destroyed $5 trillion of value.

So, what does it mean to destroy $5 trillion? Didn’t that money go somewhere? Even if a founder got rich before her company crashed, she must have gained the money to spend somewhere – real estate, vacations, champagnes and so on. If money went back in the system, how exactly did value get destroyed? As Warren Buffet explains in this article, “value is destroyed by any business that makes losses in its lifetime”. Taking to the extreme, for example, if I start a business where the whole proposition is to pay employees for sitting idle, I’m destroying value. That’s because if my business didn’t exist, those employees would have been employed elsewhere, would have still gotten paid (so they can buy stuff) AND would have been creating something of value for other people. By not making people create something of value, I’m destroying value. They’re consuming but not giving back. This means inefficient businesses destroy value. Flop movies destroy value. Bad plans destroy value. Irrational exuberance destroys value.

In other words, a startup is in the business of creating value. Full stop.

If you are an entrepreneur and all that reading about exotic business models (aka Zenefits) or loss-making growth (aka most public SaaS companies) or hoped-for-advertising profits (aka Twitter) overwhelms and confuses you, take a deep breath and simply think about the fundamentals: are those startups better at creating value for a group of humans than anyone else in the world? How large is the group of humans who benefit? And by value, you clarify: are they in a business of creating something that other people want.

To reiterate, I’ll quote Paul Graham from his essay “How to make wealth“:

‘Wealth (value) is not the same thing as money. Wealth is the fundamental thing. Wealth is stuff we want: food, clothes, houses, cars, gadgets, travel to interesting places, and so on. (To create wealth), you just have to do something people want.’ ~ Paul Graham

Closing thoughts: on future

I’ve been thinking about future of startups or economy in general. If we fast forward a 1000 years, how will our economy look like? Will we have the concept of money? There are two points worth exploring. The first one is that all the technological progress means that poverty is reducing everywhere and because of increased automation and productivity,

people’s needs are increasingly fulfilled using less cost and resources ...Read the entire post →

As the founder of a profitable software company, I happen to make more money than most office-goers of my age. There’s no shame or pride in admitting that. I don’t dislike money. Having quite a bit of it is simply a fact. Though there must be many thousands of people who have enormously more money than me, I consider myself lucky to have more than I need right now.

However, more than the money, what fascinates me is the nature of money, its ubiquity and how our behavior gets unknowingly influenced by it.

The insecurities attached with the money

I have grown up in a typical middle-class household where one is rightly nurtured into not being extravagant. I was taught to value money (which I thoroughly appreciate). Even though, in my childhood, I always got whatever I wanted, the truth is that I never wanted big, expensive toys. That attitude has lingered on to the present day. Now I know what matters and what doesn’t. I firmly believe that material possessions may end up owning my life rather than I owning them. I would certainly be not happier if the entire day I worry about my new scratch-less Porsche, my next investment or whether my portfolio is currently showing positive or negative returns.

A life spent mostly hoarding money and possessions is a wasted life

Keeping the things you own in a good condition and actively managing and cleaning them is one aspect. The other aspect is the constant worry of losing it all.

Isn’t it funny that one first works hard to earn some money, and then worries constantly about not having it anymore? This insecurity keeps even the richest people actively working to make even more money, while they sweat away their only life, working extremely hard while deprioritizing their friends / families (which of course they will regret at their deathbeds). All this hard work is for the future, though. When will this future arrive, they don’t know. With enough money in the bank, they will feel safe. Except that rarely anyone defines “enough” and no body ever is really safe. A bus could run over you tomorrow, and no amount money could save you if you were destined to die.

It’s true that having money is a good thing, and that if you happen to afford good (and probably expensive) medical treatment, chances of you surviving a crash might be higher. However, I can bet that this life-saving amount would be much lesser than what most people aspire for to “save”. And there’s always medical and disability insurance to take care of this scenario.

Then why do we run after money?

I feel there is an irrational attraction which humans have for security. They are inherent afraid of their mortality and subconsciously or otherwise, will do anything that assures them of a meaningful, comfortable existence. Money is perhaps the best proxy for this permanence that we desire. It might also be related to our evolutionary instinct of hoarding food for the rainy days. Better to have more food than less food, right?

Luxury lifestyle and the hedonic adaptation

People who make a lot of money too soon such as entrepreneurs or lottery winners usually end up increasing their standard of living. Consider how going to expensive restaurants, watching movies on a bigger TVs, or moving into a larger home would make you happy only for a while. After that initial rush, it’s back to normal. This is called hedonic adaptation and I’m sure as we reflect, we can see that this adaptation has happened many times with us, yet we keep falling into its trap.

Some might argue that even the initial rush is worth all the money, but there are many unintended side affects of significantly changing your standard of living. You end up not hanging out with your friends that often because they won’t go into that expensive restaurant. You end up spending a lot of time managing whatever things you’ve bought. You end up feeling bad about yourself because now your comparison is with houses much bigger than yours. But worst of all is that you end up feeling out-of-place at all the places that your earlier avatar once considered luxury, say an economy class airline ticket to Europe because now you prefer traveling business class.

Isn’t it ironic that just because you’re used to a better standard of life, you’ve suddenly excluded so many potential joy-bearing experiences? Sadly, some people never experience this non-correlation between money and happiness, and they end up dedicating their lives to making money while they could have had been much more happy chasing experiences. Money in the bank has rarely given anyone any happiness. All it has given is a false sense of security.

I am glad that my previous blog post Sorry, your “cool” webapp is probably not going to make money received good response and generated a lot of debate. What I discussed in that blog post was that most of the so called startups or webapps which are based on “game-changing” or “cool” ideas never end up making any money. So, if your aim is to make money, pursuing such ideas can be risky. While idea-driven startups rarely make money, I professed market-driven approach for someone looking to find startup ideas that actually make money.

Market-driven approach to finding startup ideas that make money

The market-driven approach is quite simple. It essentially means:

Sorry for crushing your dreams but your web app for tracking happiness levels (or for “social-aware” todo lists) is probably not going to make enough money to let you retire in Hawaii. Many programmers and web developers find making a web app very satisfying and there is nothing wrong with that. As long as you are doing it for fun, it is OK. But making web apps is the trivial part. After all, most web apps are nothing more than a slick interface for CRUD operations. The key to making money is to find a market where people are willing to pay for those simple CRUD operations.

The usual approach for making web apps (or “startup” as some would like to call it) is this:

Have a “cool” idea

Implement it in X number of hours

Try to justify its need by finding users who may use it

I am just making up a statistic here, but I have seen 9/10 efforts losing hope after the third step and the web app just languishes with the creator given up on it after initial euphoria.

That is a wrong approach.

If making money is the objective, I suggest going with the market-first approach (as opposed to idea-first approach). If you are confident that you will be able to make a good enough product/prototype, I suggest taking the following approach:

Find an industry (ideally, an old fashioned one) where people are making money

Find the single differentiator which will put your app apart in the already established industry (read or research what pain points are still not addressed by top 3 solutions)

Make a web app, market it, refine it based on feedback, monetize the app

Slowly incorporate all standard features expected out of a solution in that industry so you can shoot to be a market leader

I admit it: my previous (so called) “startup” Kroomsa was a failure. Back when I was starting up, I remember how game changing I thought it was. We wanted to revolutionize Indian music scene by inserting audio advertisements into music. We also vowed to donate 20% of proceeds from advertisements to a charity organization. Do you see how cool the idea was? Though this business, we combated piracy of music, made money for independent bands and helped society by supporting charities. All at once!

Except that we never made a penny out of the venture. First mistake: none of the team members was doing it full time. Second mistake: none of the team members had any experience in music industry. Third and biggest mistake: the idea was “cool”. To my hacker brain, this crazy business model was like dope. I distinctly remember being on a high for several days when I initially thought of that idea.

According to my then interpretation of “execution is important than the idea”, I started implementing the business model without doing any reality check at all. I built the music platform, roped in friends to help me, contacted a few initial music bands, uploaded music and added a dummy advertisement in songs! Before I realized my project was a startup. As time passed, I realized:

Nobody likes to listen to advertisements in songs. In fact, people hated it. Lack of basic market research.

Nobody in India likes to pay for music, let alone for independent rock music. Market was tiny.

With no experience in music or corporate industry, we had no clue how to bring in advertisers. Lack of business and marketing plan.

Finding good bands and signing them up was a non-scalable, extremely laborious task. So, our inventory of music was small. That meant even if we found an advertiser, our reach wasn’t so appealing. The chicken-and-egg problem.

I thought I knew! But the more I introspected, the hazy my understanding got. Is GDP amount of stuff produced or consumed? Does it include imports or exports? What does it have to do with well being? Why does it keep increasing?

So, I fired up Claude and started understanding what GDP really is. This post contains my notes on the same.

But before we start, it’s worthwhile to reflect how many such concepts that we think we know, do we really know. Often there’s a gap between what we think we know, and what we actually know. It’s worthwhile to question your understanding of commonplace phenomena. Do we know what life is? What does productivity mean? How do greenhouse emissions warm the Earth, and so on. For so many such things, our mind convinces us that we know stuff when upon probing, it turns out to be a vague miasma. ...Read the entire post →